On your phone, download any finance app and open it; you will see the market shift clearly. People send money, pay merchants, and manage balances in seconds with just one app. For businesses, the apps are becoming a large roof where multiple things take place and a great example of the same is X Money.

To build a fintech wallet app like X money, it is not just about creating a payment tool but more of a financial layer that connects into social and business ecosystems parallelly. They are built to prepare a unified experience where transactions feel as instant and intuitive as sending a text message on both the receiver and payee sides.

But is it really to build such an app and what does it all take to build such an app? Well, the answer starts from understanding what an app like X Money solves, its features, and what it runs on.

The real-world problems that an app like X Money eliminates

Earlier, the traditional financial system was stuck with fragmentation, where social interactions and financial transactions took place in different places. It means users as well as businesses had to juggle between messaging apps and banking portals to settle a bill.

This app fatigue bought a notable amount of barrier to entry for modern consumers and X Money studied that. Not only was it studied, but it was also removed by building a financial service that easily blends into the daily social activity.

It gave a single ecosystem where users can chat, shop, and store funds to remove that fragmentation problem. For founders who want to develop app iOS and Android versions of such a product, the inspiring stuff is removing the multi-step hurdles of cross-border transfers and merchant payments. X Money solves this by coming up as a digital value that connects to a global payment network where transactions are verified in milliseconds instead of days.

Further, the platform also solves the trust gap, as many users hesitate to adopt new payment platforms that lack clear transaction records or transparent dispute resolution. X Money builds this trust with real-time transaction history, instant push notifications, and a transparent ledger architecture. For businesses it solves the onboarding nightmare with automated KYC and AML processes so that merchants can start accepting global payments instantly.

In a nutshell, the common problems that X money solves are the following:

- Payment siloes by merging communication and payments into one interface.

- Merchant Onboarding Delays: With automated systems that reduce the time it takes for a business to go live.

- Cross-border complexities that simplify international transfers using multicurrency support and real-time exchange rate calculations.

- Lack of financial transparency with exportable statements and activity logs that support fast dispute resolution.

The core and advanced feature sets that go into apps like X Money

If you plan to compete in the modern fintech world, a digital wallet should not be just a simple payment tool but more of a full ecosystem of finance. The modern users expect more than just the ability to store money, something they can use for commerce, social interaction, and wealth management without any problems.

When you set out to build such an app, your feature roadmap determines if your product becomes a daily essential or just another icon in a crowded finance folder.

The must-have MVP features

- Every successful wallet starts with a core set of features that guarantees basic usability and trust. The below forms the backbone of your initial launch:

- Secure Onboarding and KYC: A step to not ignore as it consists of verifying documents, facial recognition, and risk scoring to meet global Anti Money Laundering standards.

- Wallet balance and transaction management: This is one dashboard where users can see balances, track movements of funds and access immutable transaction logs, all at a single place.

- Peer-to-peer transfers: This lets users send or request money instantly either with help of usernames, phone numbers, or contracts as per their inconvenience.

- Multi-source payment integration: It allows users to link debit cards, credit cards, or bank accounts using secure APIs to fund their digital vault.

- QR and merchant payments: Support for contactless retail transactions, which has become a global standard for modern digital payments.

The advanced features for unique value

While core features deliver utility, advanced capabilities are what truly separates a platform and drives user retention. This is where the strategic focus of fintech wallet app development shifts towards building a super app experience.

- Subscription and recurring billing: Automated management of SaaS plans, membership tiers, and trial periods to create predictable revenue streams for businesses.

- Custom card issuing: Powering the users and businesses to issue their own branded physical or virtual debit cards with genuine spending controls.

- Creator Monetization and Instant Payouts: A special tool for the creator economy that includes tipping services and automated revenue splits between platforms and creators.

- Crypto and Digital Asset Support: A crypto wallet lets users’ invoice, store, and transfer digital assets like BTC, ETH, and stablecoins along with fiat currency.

- AI-powered fraud prevention: Making use of machine learning models to find user behaviour in real time with risk scores for transactions before funds are even moved.

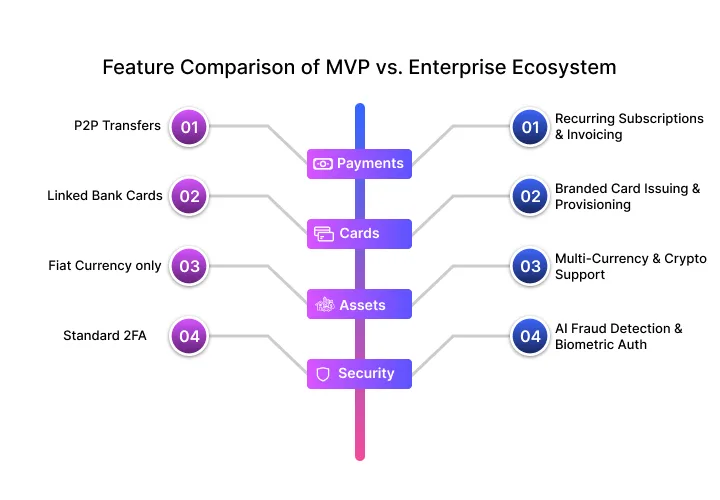

Feature Comparison of MVP vs. Enterprise Ecosystem

| Feature Category | Basic MVP Wallet | Enterprise Ecosystem (X Money Style) |

| Payments | P2P Transfers | Recurring Subscriptions & Invoicing |

| Cards | Linked Bank Cards | Branded Card Issuing & Provisioning |

| Assets | Fiat Currency only | Multi-Currency & Crypto Support |

| Security | Standard 2FA | AI Fraud Detection & Biometric Auth |

The business model of platforms like X Money

To build such a world-class fintech app requires some notable investment but the right monetization strategy changes it from a cost center to a high-yield revenue engine.

Platforms like X Money rarely go for a single income source, as they layer multiple financial services to generate steady, predictable cash flow while giving immense value to both individual users and global merchants.

Transaction and Merchant Fees

The key driver for most digital wallets is transaction and merchant fees. Wallet platforms act as a payment gateway for businesses where they charge a small percentage (around 1% to 3%) on every transaction they process.

You can also go for spreading the charges as per currency; like for EUR and GBP, you can go for 1%, whereas for USD and RON, you can charge 1.5%. These small fees accumulate quickly when a platform processes millions of ledger updates daily.

Currency Exchange Margins

More than just simple payments, savvy founders look at currency exchange margins. For international transfers, apps earn revenue where they apply a small markup on the market exchange rate during conversion. This is great in a globalized economy where cross-border payments are a standard requirement for businesses.

Subscription-Based Revenue

With the rise of embedded finance, you can offer advanced infrastructure like automated recurring billing for SaaS companies or membership sites. The platform creates a predictable revenue model for itself and its clients and displays the most feasible option to them.

For a better evaluation, you can partner with mobile app development services in India, who will help you understand the model since, being a global hub for innovation, the companies from here work with global partners and can suggest your diverse streams.

Common Revenue Streams for Fintech Wallets

| Stream | Description | Growth Potential |

| Transaction Fees | Percentage-based fees on P2P or retail payments | High (Scales with user volume) |

| Merchant Charges | Fees for providing payment infrastructure and QR tools to businesses | Stable (Long-term business contracts) |

| FX Margins | Profit from currency conversion markups when a user does global transfers | Variable (Dependent on cross-border traffic) |

| Premium Tiers | Subscription plans that give users more than normal that is high limits, less fees, and access to some more advanced analytics. | Predictable (Recurring monthly revenue) |

A Step-by-Step Development Roadmap for an app like Money X

Moving from a vision on a whiteboard to a fully functional fintech ecosystem like X Money requires a structured, disciplined engineering path.

You cannot simply build a wallet; you must architect a safe financial institution in digital form so that every transfer follows a strict security protocol before the product goes live.

Phase 1: Discovery and Market Validation

Take a look at any product, the first step to their success was the research part. In this phase, teams define payment streams, user segments (consumers, merchants, or creators), and the core functions required for the first release. This is where the product roadmap is solidified after identifying exactly which friction points your app will solve first.

Phase 2: UX Design and Payment Flow Mapping

In fintech, simplicity is the ultimate security. Designers focus on mapping payment flows that feel simple even though the underlying system is incredibly complex. Important screens consist of user onboarding with identity verification, real-time wallet dashboards, and intuitive payment initiation interfaces.

A cluttered interface kills engagement instantly as users expect transactions to feel as easy as sending a message.

Phase 3: Core engineering and the power of choice

The choice of tech stack plays a big role in deciding how fast you can launch and how much you will spend for the maintenance of the product.

For modern businesses, the choice is generally cross platform development with Flutter or React Native because it lets them deploy products on iOS and Android without writing a separate codebase.

When it comes to backend, a microservices architecture is going to work well for fintech apps as it lets modules like payment processing, KYC verification and notifications run independently.

This setup makes the system easier to scale and capable of handling millions of transactions on a daily basis with downtime.

Phase 4: Banking Integration and Financial Rails

A digital wallet cannot work without connections to traditional financial institutions. This phase consists of integrating with card payment processors like Stripe or Visa Direct, bank account connection APIs like Plaid, and real-time payment networks to allow instant fund movement.

Phase 5: Security, compliance, and constant testing

Security should never be a negotiable aspect when it comes to fintech. This stage consists of applying PCI DSS Level 1 standards, asset tokenization to protect card data, and AI-driven fraud detection to find user behavior in real time.

Before launch the system must undergo transaction simulation, where strict testing for load capacity, payment failure recovery, and security vulnerabilities takes place.

Phase 6: Launch and Platform Expansion

For the first release, the team can keep their focus on core payment functionality and basically the user onboarding. Then once live, teams get further user data and begin expansion of advanced features like merchant ecosystems, international payment support, and digital asset management.

What Does It Actually Cost to Build the Next X Million?

Preparing a budget for a fintech project requires a balance of high-end security infrastructure with a seamless user experience. While costs vary on the basis of the complexity of your features, opting for mobile application development in India allows you to utilize world-class engineering talent at a fraction of the cost in North American and European markets.

| App Type | Estimated Cost Range in USD with higher side | Included Key Features | Ideal For |

| Basic MVP Wallet | From $20,000 to $60,000 | Features like user onboarding with KYC, linking of bank as well as card, P2P transfers and basic notification system | Startups validating their idea of a niche payment product in early markets |

| Advanced Wallet Platform | From $50,000 to $150,000 | Features like advanced ID verification, constant monitoring for fraud with AI, QR payments for merchants, and all the processing in real time. | Growing fintechs or neobanks ready to expand their service ecosystem |

| Enterprise Wallet Ecosystem | From $100,000 – $250,000+ | Features like payouts for creator, support for multiple currencies, risk scoring with AI, and analytics dashboards with all advance metrics | Large Scale institutions that can handle millions of users and global transactions |

Round up with a few more words

The fintech wallet app development is going to be a complex journey but the rewards in the end are worth the time and investment. Keep in mind that the key is to build an entire financial ecosystem with best of convenience, speed and security because this is what users want in place of generic wallet apps.

When your product goes into its first discovery workshop, keep the regulatory compliance in mind because that is where a lot of fintech startups fail to consider. While you look for a fintech development partner, go for India because it is going to be the most cost-effective option for you. And, last but not the least, success in this market comes to the ones who invest in scalable architecture and a seamless user experience.