The United Arab Emirates is becoming an inspiration as a global hub for financial innovation where a national vision for a digital-first economy is playing a key role. But as the volume of real-time transactions becomes massive, so do the risks of fraudulent networks going big.

Traditional rule-based security measures are no longer sufficient to counter these ongoing threats. As a result, financial institutions are shifting towards intelligent, automated systems to safeguard the integrity part and maintain institutional trust.

This transformation requires existing finance as well as young or in-development-phase firms to understand the latest trends ongoing in the AI financial fraud detection space.

The UAE Fraud Ecosystem by the Numbers

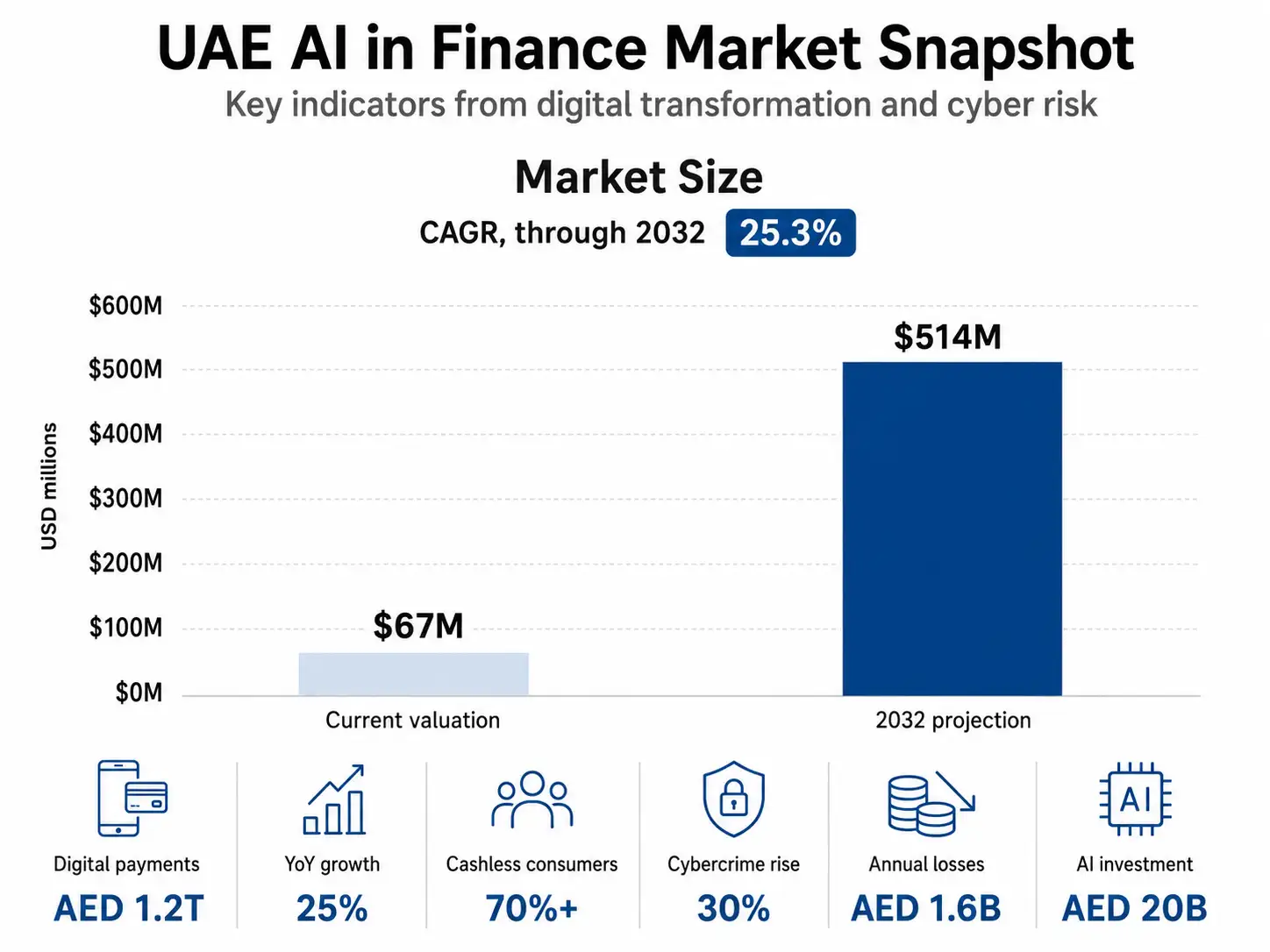

The scale of the digital transformation in the Emirates is best shown by the surge in digital payment transactions, which has recently arrived at AED 1.2 trillion, which reflects a 25% year-on-year growth.

With over 70% of consumers going cashless for transactions, the surface area for cybercrime is also opening up. At the current time, the UAE has seen a 30% rise in cybercrime incidents, where annual losses have crossed AED 1.6 billion.

To solve such risks, a lot of institutions are going with custom AI solutions to find complex anomalies that traditional human analysts might miss. The market for AI in finance is expanding aggressively; even if the current valuation a couple years ago was at USD 67 million, the projects are to reach USD 514 million by 2032. This growth rate will be 25.3% annually.

And the growth is backed by government-based investment in AI technologies that again is going to cross the investments of AED 20 billion.

The Challenge of Implementation

While demand for a specialized AI-powered application is at record highs, implementation remains a major challenge. The initial setup for a mid-sized financial institution can even cross AED 2.5 million, with ongoing maintenance costs adding another AED 600,000 annually.

Further, the market is notably alarmed by the skills gap, with an estimated shortage of 25,000 AI and cybersecurity professionals in the UAE. This talent difference often forces institutions to look for external expertise to explore the complex technological requirements of modern fraud detection.

The internal teams struggle to maintain 45% better rates in detection effectiveness without AI support.

Trend 1: The shift to Explainable AI XAI

The shift from black box models to regulatory clarity

One of the troublesome problems in the adoption of machine learning for fraud detection is the black box nature of deep learning models. These systems just flag transactions without any clear reasoning, which creates accountability issues for auditors and compliance officers.

In the UAE, the Central Bank (CBUAE) and the Abu Dhabi Global Market (ADGM) have clear strict transparency requirements. If an entity is unable to justify a fraud alert, it can lead to legal and reputational risks.

With that, the sector is shifting towards modern banking with Explainable AI XAI to make sure that every automated decision is auditable and justifiable.

The role of SHAP and LIME in auditability

To meet transparency standards, financial institutions use tools like SHAP and LIME. These tools explain how AI models make decisions by showing which factors matter most — for example, a sudden change in location or an unusual transaction time. It lets human analysts understand why the AI reached a given conclusion.

Forward-thinking firms are now going with AI and GPT integration services providers to convert these complex technical scores into natural language summaries that make it easier for non-technical stakeholders to review and verify high-risk alerts.

Hybrid Architectures for Accountability

UAE banks are adopting hybrid models that combine the predictive power of machine learning with rule-based expert systems. This approach lets institutions maintain the high detection accuracy of AI while making sure that specific non-negotiable regulatory rules always stay in compliance.

Research shows that this balance of strategy has given a 45% improvement in fraud detection effectiveness across the region. It is because it actively contributes in building institutional trust and aligns the vision of the UAE’s government about strong data protection.

Trend 2: Graph Neural Networks or in short GNNs

The hidden collusive networks

Big level fraud schemes like money laundering and synthetic identity fraud mostly have organised rings that share illicit activities across hundreds of interconnected entities. Traditional machine learning models struggle here because they generally treat each transaction as an isolated event.

Graph Neural Networks (GNNs), however, show financial data as a structured network where entities (customers and merchants) are nodes and transactions are edges. This allows the system to analyse the relational dependencies between entities and identify multi-hop transaction loops that indicate layering or collusive behaviour.

Benchmarking Performance: GAT v. Traditional Models

From empirical benchmarks, they have shown the superior performance of GNN architectures like Graph Attention Networks compared to classical algorithms. While traditional methods like XGBoost may achieve a recall of only 72%, GAT models have shown a recall of 91% and an overall accuracy of 95% in detecting complex fraud patterns.

This shift in precision is a basic driver for the emergence of agentic AI in financial services, where autonomous AI agents can actively explore these transaction graphs. They can identify and freeze the whole clusters of fraudulent nodes before they can complete a cash-out phase.

Real-time feasibility and scalability

A common problem with graph-based models is their computational intensity but recent optimisations have made them viable for high-frequency UAE payment platforms. Techniques like GraphSAGE (graph sample and aggregate) use neighbourhood sampling to notably reduce processing time without sacrificing accuracy.

For example, inference speeds as low as 2.8 milliseconds per transaction have been recorded for these models so that real-time security does not introduce friction into the digital customer experience.

Trend 3: Behavioural Biometrics and Real-Time Analytics

From static credentials to continuous authentication

As fraudsters can easily bypass traditional multifactor authentication, UAE financial institutions are moving to behavioural biometrics to add a layer of invisible security. It is not like physical biometrics because it studies the user’s rhythm, mouse movement patterns and touch screen pressure.

With constant monitoring of these interactions in a session, AI systems can find account takeover or ATO attempts even if the attacker has made the login correct. This shift shows a move from usual authentication to continuous authentication so that the person behind the screen is only the one and real account holder.

The computational efficiency of real-time monitoring

The primary challenge for regional payment platforms is processing these behavioural streams without introducing transaction latency. Modern architectures now utilise optimised inference models that can evaluate thousands of data points per second.

For instance, specific AI-driven fraud detection frameworks have achieved inference speeds as low as 2.8 to 4.1 milliseconds per transaction.

This constant processing lets banks move from reactive investigations, which often occur after losses are incurred, to proactive prevention where suspicious transfers are frozen before they leave the ecosystem.

Many institutions are now engaging in AI development consulting to customize these high-speed models to their specific user bases so that local behavioural nuances like multi-language input styles common in the UAE are accurately represented in the training data.

Benchmarking Detection vs Customer Friction

Effective behavioural models are evaluated not just on their detection rate but also on their ability to minimise false positives, which can be costly and damaging to customer relationships. High-accuracy models like multi-layer perceptrons (MLPs) have shown precision rates as high as 92.6% in identifying fraudulent instances.

As we lower the number of legitimate transactions flagged as suspicious, banks can deliver a frictionless experience. Some that act as differentiators in the UAE fintech market where 70% of consumers have gone digital first.

Trend 4: Hybrid Models and Regulatory Tech

Bridging the accuracy explainability gap

The UAE regulatory environment, led by the Central Bank (CBUAE), increasingly mandates that AI systems be both accurate and interpretable. To satisfy these dual requirements, the industry is moving towards hybrid models that bring deep learning algorithms with traditional rule based expert systems.

This mixed approach lets AI find new fraud patterns, while the rule‑based system makes sure that strict compliance with regulatory thresholds is present.

Automating Compliance Workflows

The surge in digital transactions recently hitting AED 1.2 trillion has made manual compliance audits physically impossible for human teams to manage alone. AI-driven RegTech solutions now automate the generation of audit-ready reports that translate complex risk scores into natural language justifications for regulators.

Research indicates that these automated workflows have led to a 45% improvement in fraud detection effectiveness for Middle Eastern banks by allowing compliance officers to focus on high-priority alerts rather than routine data entry.

Given the complexity of integrating these systems with legacy banking infrastructure, there is a rising demand to hire AI developers in Dubai who specialise in regional compliance standards. These experts make sure that AI models are trained on diverse datasets that reflect local transaction habits while adhering to the UAE’s national cybersecurity strategy.

Partner with NetSet Software: a leader in AI FinTech app development

Navigating the intersection of cutting-edge AI and the UAE’s rigorous financial regulations requires a partner with deep technical and regional expertise.

As a premier AI fintech app development company, we specialise in building secure, scalable and compliant fraud detection systems that protect your assets while making the user experience better.

Whether you need graph neural networks to uncover collusive fraud or explainable AI XAI to satisfy CBUAE requirements, our team is ready to turn your security strategy into a competitive benefit.

FAQs

How does AI do better fraud detection if we compare it with older methods?

When it comes to old methods, they were mostly rule based who worked on static information that was too easy for a hacker to guess and bypass. Now with the power of AI models like Graph Attention Networks or GAT, the system understands the relationships between entities.

What is Explainable AI (XAI) and what is its importance when it comes to the UAE region?

It converts machine learning decisions into justifications that can be read by humans and in UAE regulators like the CBUAE and ADGM ask financial institutions to give traceable reasoning if there are any flagged or blocked transactions.

Can AI-driven fraud detection work in real time?

Yes, there are modern sampling techniques like GraphSAGE that models process complex transaction data in as little as 2.8 milliseconds so that security checks do not slow down the customer experience.

What are the main costs when it comes to having AI for fraud detection?

If we talk about mid level institutions, initial setup costs can exceed AED 2.5 million with annual maintenance having an average of AED 600,000. But the 45% increase in detection effectiveness and reduction in fraud losses often prove itself as a strong ROI.

How does behavioural biometrics protect my account?

It continuously studies how users interact with apps, like their typing rhythm and mouse movements and in case any unauthorized user gains password but types differently than user, the AI can detect and freeze the session in real time.